To run payroll and accounting around HMRC compliance deadlines you will need to invest in creating structured processes that will streamline and ensure timely payroll submissions, payment of taxes, VAT returns, and statutory filings. For your practices it’s important to stay one step ahead of deadlines to avoid penalties and unnecessary stress for your clients and bad reputation for your practice.

For instance, a practice was facing a new deadline every month related to PAYE submissions, pension contributions, VAT returns, payroll processing, and year-end accounts. The practice was stuck between a constant struggle to meet the deadlines while addressing last-minute client requests.

One time, the client sent payroll information late, which created a chain reaction that affected RTI submissions and payroll processing. While it was resolved, this problem could have been avoided if there had been proper planning.

The practice invested in structures like compliance calendar, automated key workflows, and introduced regular client reminders. The result was fewer last-minute surprises, improved efficiency, and better client service.

In this guide, we’ll explore how accounting practices can plan payroll and accounting activities around HMRC deadlines, reduce payroll compliance risks, and create more efficient workflows.

Understanding HMRC Compliance Deadlines

HMRC compliance is not limited to just tax return filing one a year. When you handle HMRC compliance for your clients, your team of accountants have to deal with multiple deadlines throughout the year, including payroll submissions, tax payments, VAT obligations, and corporation tax requirements.

Some of the most important deadlines include:

PAYE and Payroll Deadlines

Clients operating PAYE must submit payroll information through Real Time Information (RTI) on or before the employees are paid.

Key payroll obligations include:

- Full Payment Submission (FPS)

- Employer Payment Summary (EPS), where applicable

- PAYE and National Insurance payments

- Pension contribution reporting

The PAYE bill must be paid to HM Revenue and Customs (HMRC) by:

- The 22nd of the next tax month, if you pay monthly

- The 22nd after the end of the quarter, if you pay quarterly – for example, 22 July for the 6 April to 5 July quarter

If you pay by cheque through the post, it must reach HMRC by the 19th of the month.

VAT Deadlines

All your clients whose are running businesses and their turnover exceeds £90,000 in a rolling 12-month period will have to submit their VAT returns and make payments as per the reporting schedule.

The deadline for submitting VAT returns online is usually one calendar month and 7 days after the end of an accounting period. This is also the deadline for paying HMRC.

Corporation Tax Deadlines

Companies generally need to:

- Pay Corporation Tax within 9 months and 1 day after their accounting period ends.

- Submit a Corporation Tax Return (CT600) within 12 months of the accounting period end.

Self-Assessment Deadlines

Business owners, directors, and self-employed individuals may also have personal tax obligations requiring careful planning. Missing any of these deadlines can result in penalties, interest charges, and unnecessary administrative burdens.

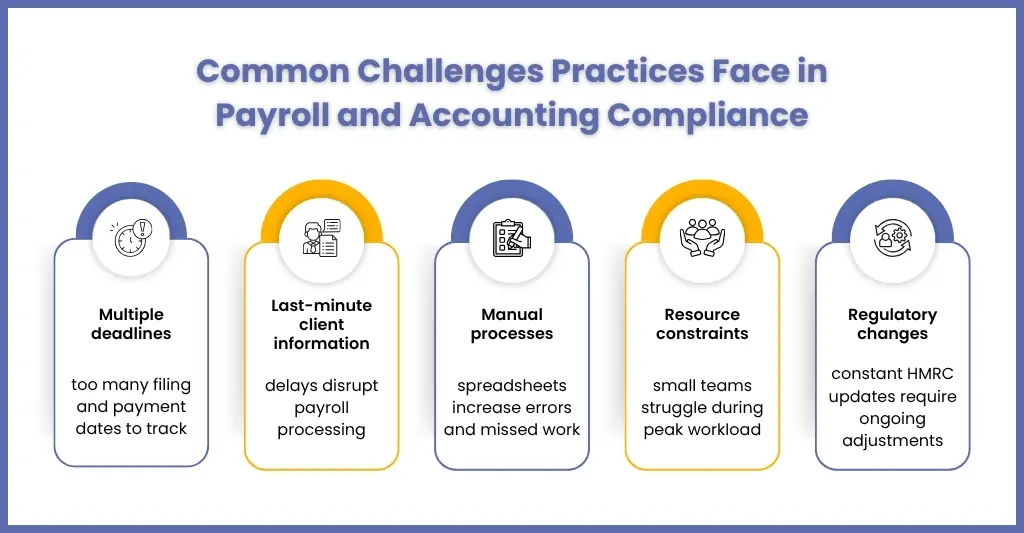

Common Challenges Practices Face in Payroll and Accounting Compliance

Even after knowing the importance of maintaining compliance with HMRC payroll and accounting deadlines, we have found practices struggling with meeting them due to multiple challenges. Let’s understand each of the common challenges.

Managing Multiple Deadlines

One of the biggest hurdles in the path of maintaining compliance with HMRC deadlines is keeping track of numerous filing and payment dates.

You will have to manage:

- Weekly payrolls

- Monthly payrolls

- Quarterly VAT returns

- Annual accounts

- Corporation Tax returns

- Self-Assessment deadlines

Without advanced planning important dates can be easily missed.

Last-Minute Client Information

You might have missed on deadlines due to delayed communication from your clients.

The client has to provide critical information, such as:

- Payroll changes

- Employee information

- Expense records

- VAT documents

When this information is provided at the last minute, it leaves your accountants with limited time to process the information accurately.

Manual Processes

It will be hard to believe, but we have found a few practices still relying on spreadsheets and manual workflows. It increases the risk of:

- Data entry errors

- Missed deadlines

- Duplicate work

- Compliance mistakes

As client numbers grow, these inefficiencies become more significant.

Resource Constraints

Recruitment of accounting talent in the UK is a big challenge, and getting expert talent is neither easy nor reasonable. Many practices operating small accounting teams and try to manage increasing compliance demands. As a result, staff get overwhelmed during peak seasons, which increases the chances of human errors.

Constant Regulatory Changes

UK payroll and tax regulations are constantly evolving.

Keeping up with:

- PAYE changes

- National Insurance updates

- Pension requirements

- HMRC guidance

requires continuous monitoring and training.

Step-by-Step Plan to Align Payroll and Accounting with HMRC Deadlines

The only way to overcome the above challenges in meeting compliance with HMRC payroll and accounting deadlines is proactive planning.

Here’s a practical framework that accounting practices can follow.

Step 1: Create a Master Compliance Calendar

Create a calendar that centralises all the deadlines. It should include:

- Payroll processing dates

- RTI submission deadlines

- PAYE payment dates

- VAT deadlines

- Corporation Tax deadlines

- Accounts filing dates

- Self-Assessment deadlines

A centralised calendar provides visibility across the entire practice, leaving no scope for confusion.

Step 2: Build Internal Deadlines Before HMRC Deadlines

It would be counterproductive to wait until the official deadline; it will only lead to rushed work and increased chances of errors. Instead, establish internal deadlines several days before submission dates.

For example:

- Client payroll information due by the 20th

- Payroll processing is completed by the 25th

HMRC submissions completed before the official deadline. This creates a buffer for unexpected issues.

Step 3: Standardise Client Communication

Most compliance problems occur because your clients don’t know what information you provide and when.

Therefore, create standard communication processes such as:

- Monthly payroll reminders

- VAT document requests

- Year-end information checklists

Through clear communication, delays are avoided and accuracy improves.

Step 4: Automate Where Possible

Automate all the tasks that can be automated, especially repetitive ones, so that the workload is reduced.

Modern payroll and accounting systems can automate:

- Payroll calculations

- RTI submissions

- Client reminders

- Payroll reporting

- Workflow tracking

Various studies show that payroll automation reduces manual processing time while helping organisations improve compliance consistency.

Step 5: Conduct Regular Compliance Reviews

Don’t conduct reviews to identify issues at the end of the year. Conduct frequent reviews, quarterly one to ensure:

- Payroll records remain accurate

- VAT obligations are met

- Tax liabilities are understood

- Compliance risks are identified early

Such regular reviews support better decision-making and minimise surprises.

Step 6: Develop Contingency Plans

Always build some contingency plan to cater to unexpected events that can disrupt compliance processes.

Examples include:

- Staff absences

- Software issues

- Client delays

- Cybersecurity incidents

A well-written contingency plan helps maintain continuity when challenges arise.

Tools and Resources to Simplify Compliance

Handling so many deadlines along with catering to clients’ demand for reports, services, and insights is not humanly possible. You will need tools and additional resources for handling compliance effectively.

Payroll Software

A modern payroll software can automate:

- PAYE calculations

- RTI submissions

- Pension processing

- Payslip generation

Cloud Accounting Platforms

Solutions such as Xero, QuickBooks, and Sage provide:

- Real-time financial visibility

- Automated bank feeds

- VAT reporting functionality

Workflow Management Systems

Many practices have started using practice management software, which can help you in:

- Tracking deadlines

- Allocate tasks

- Monitor progress

- Improve accountability

HMRC Resources

Official HMRC sites frequently publish updates on tax rates, deadline changes, guidance, and compliance information. These sites must be monitored to avoid non-compliance.

Combining technology with structured processes creates a stronger compliance framework.

Real-World Example: How Practices Avoid Penalties

An accounting practice managing payroll and bookkeeping of 30 SME clients was meeting their deadlines using spreadsheets and email reminders.

As the client base grew, problems emerged:

- Late client submissions

- Missed follow-ups

- Increased stress around payroll periods

The practice implemented:

- A central compliance calendar

- Automated client reminders

- Cloud payroll software

- Monthly workflow reviews

Within six months, payroll processing became more predictable, deadline compliance improved, and staff spent less time chasing information. More importantly, the practice reduced the risk of penalties and improved client satisfaction.

This example demonstrates that compliance success often comes down to planning and process improvements rather than simply working harder.

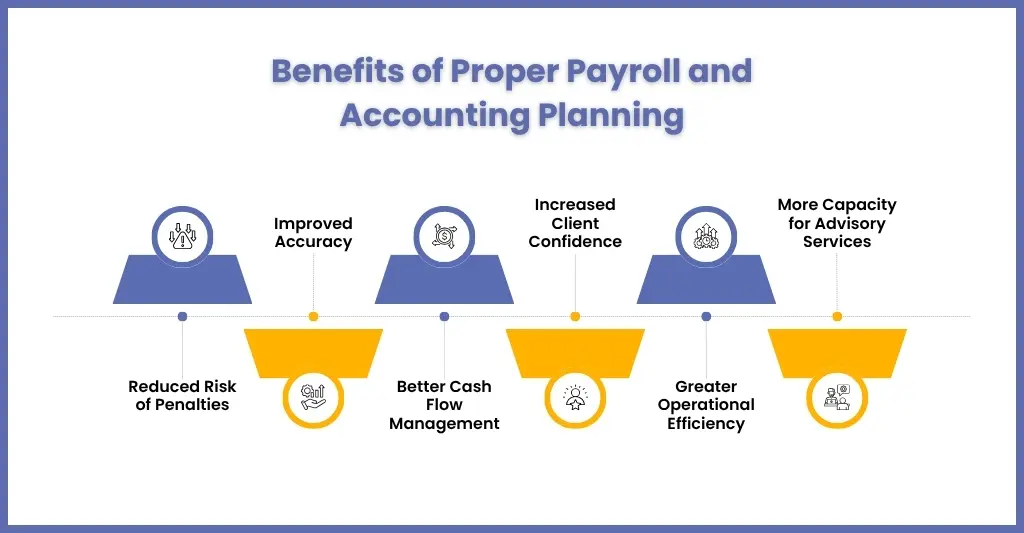

Benefits of Proper Payroll and Accounting Planning

Having a proper payroll and accounting plan will benefit both you and your clients. Some of the major benefits are:

Reduced Risk of Penalties

Meeting deadlines consistently helps you avoid:

- Late filing penalties

- Interest charges

- Compliance investigations

Improved Accuracy

With planned workflows in place that achieve deadlines with a buffer time, it will reduce panic among your clients and inside your team, avoiding rushed processing and minimising errors.

Better Cash Flow Management

Through proper payroll and accounting planning, you will understand tax liabilities better enabling you to provide your clients with insights that will help them financially.

Increased Client Confidence

Planning gives you high insights and tools to provide high-value support to your clients, which will be highly appreciated, increasing their trust in you.

Greater Operational Efficiency

Without payroll and accounting planning, your accountants will be bogged down with firefighting multiple deadlines, instead of focusing on high-value services.

More Capacity for Advisory Services

As compliance processes become more efficient, you can dedicate more resources to:

- Tax planning

- Business advisory

- Forecasting

- Growth support

This shift is increasingly important as clients seek more strategic guidance from their accountants.

Many firms are achieving this by combining technology with outsourced support from professional providers like Corient. Through a reliable payroll outsourcing services and many other accounting services, Corient has managed compliance workload with ease, freeing up practice’s internal resources for advisory and client relationship.

For practices that are expanding, outsourcing provides additional capacity without the challenges associated with recruitment and training.

People Also Ask

How can Accounting Outsourcing Services help with HMRC compliance?

Accounting outsourcing services can support payroll processing, bookkeeping, VAT returns, management accounts, and other compliance activities. By providing additional capacity and expertise, outsourcing partners help accounting firms meet deadlines more consistently while reducing operational pressures.

What are the most important HMRC compliance deadlines to remember?

Key deadlines include payroll RTI submissions, PAYE payments, VAT returns and payments, Corporation Tax payments, Corporation Tax Return filings, Annual Accounts submissions, and Self-Assessment deadlines. The specific dates depend on the business structure and reporting obligations.

What are the risks of missing payroll and accounting deadlines?

Missing deadlines can lead to financial penalties, interest charges, increased HMRC scrutiny, reputational damage, and additional administrative work. Repeated compliance failures may also affect client trust and business relationships.

What is the payroll processing deadline?

A payroll cutoff date is the final deadline to submit attendance, timesheets, bonuses, and deductions for processing. Any data submitted or approved after this date is rolled over to the next pay cycle. Deadlines vary based on your pay cycle and location.

What is the due date in accounting?

In accounting, a due date is the final, specific deadline by which a financial obligation, such as an invoice, loan, or tax bill, must be settled. Paying after this deadline means the balance is overdue, which can trigger late fees, interest charges, or penalties.

Conclusion

Achieving HMRC compliance in advance cannot happen without investing in payroll and accounting, which includes consistent communication, processes, and tech.

When compliance structures are in place, the risk of non-compliance with deadlines goes down significantly, and efficiency goes up. These structures have to be flexible in design to evolve with the regulatory environment so they serve your clients better, preventing penalties and creating capacity for growth.

For practices looking to scale without increasing internal pressures, partnering with a specialist outsourcing provider such as Corient can provide the expertise and operational support needed to maintain compliance while focusing on higher-value client services.

Want to stay ahead of deadlines? Contact us for effective payroll and accounting planning and transform compliance from a source of stress into a competitive advantage.