HMRC had announced the pausing of MTD for Corporation tax implementation on 21st July 2025. Yet your clients still asking questions like “Are we still supposed to prepare for MTD for corporation tax, or has that been scrapped?” It’s a similar story for every accounting practice in the UK, and it’s time to put the nail in the coffin.

Such questions are being posed by your clients because no other reform in the UK accounting sector has caused as much confusion as MTD for corporation tax. It was announced, discussed, planned, and then paused by the HMRC, giving practices a vital breathing space.

So, why did HMRC take this decision? What does the pause mean for your practice? And what should be your future course of action? All these questions will be answered in the guide below.

What Is MTD for Corporation Tax?

MTD for Corporation Tax was proposed by HMRC to expand the MTD initiative beyond VAT and Income Tax Self-Assessment. Under MTD for Corporation tax, your clients will need to:

- Keep digital records for corporation tax

- Submit corporation tax data digitally

- Potentially move towards more frequent or structured reporting

The reason for expanding MTD on Corporation Tax is the same as for VAT and ITSA:

- Reduction in errors

- Closing the tax gap, which was 15.8% or £18.6 billion in the tax year 2023 to 2024

- Modernising reporting

By bringing corporation tax under the MTD initiative, the corporation tax data would have gone through a transformation in how it is prepared, reviewed, and submitted. However, HMRC discovered that it is easier said than done.

The Policy Timeline – From Proposal to Pause

The goal of introducing MTD by HMRC is to digitise the entire UK tax regime and, through it, make it faster, more accurate, and reduce the tax gaps that are occurring in VAT, Income Tax, and Corporation Tax.

HMRC had a clear direction and implemented it properly, starting with:

- The MTD initiative was announced in 2015

- MTD for VAT launched in 2019

- MTD expanded to all VAT-registered businesses in 2022

- Expansion of MTD for Income Tax will be implemented starting April 2026

- MTD for corporation tax planned next

But in 2025, HMRC confirmed it was pausing work on MTD for corporation tax, and many industry bodies were happy with this decision. Bodies like the Association of Taxation Technicians have pointed out that the scope and complexity of corporation tax made implementation far more challenging than VAT.

Understanding the challenges associated with implementing MTD for Corporation Tax, HMRC took a step back.

Why HMRC Stepped Back from Making Tax Digital for Corporation Tax

The implementation of MTD on VAT has been beneficial on VAT and HMRC is confident about the success in Income Tax too. But HMRC has taken a step back on implementing MTD on Corporation Tax, not because it does not want to, but due to the practicality of implementing it, due to multiple challenges.

Key reasons included:

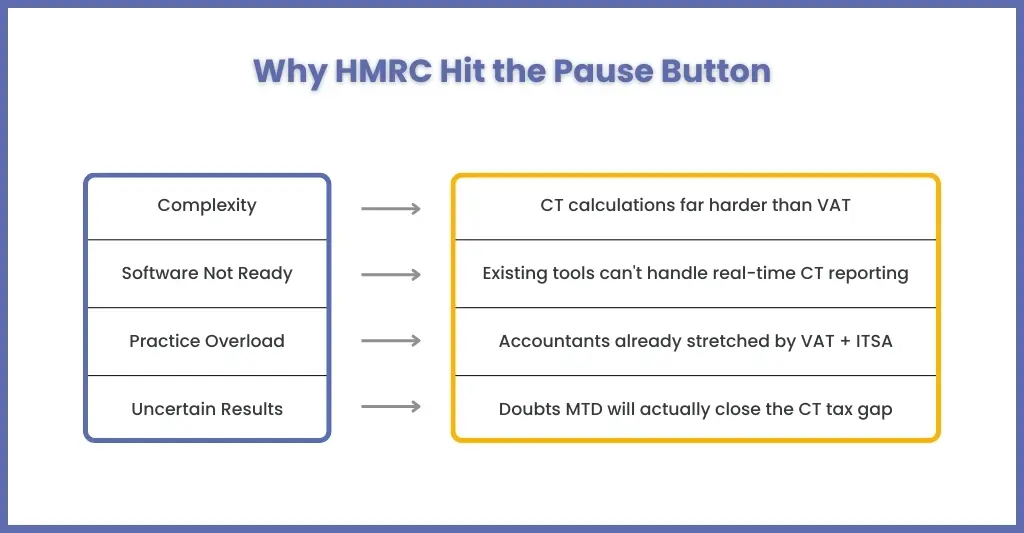

Complexity of Corporation Tax Calculations

Corporation tax rules are already complex and its calculations even more. Corporation Tax depends on multiple aspects such as year-end accounts, tax adjustments, capital allowances, losses, group relief, R&D, and more. Unlike VAT, it cannot be divided into quarterly periods.

Software Readiness

The existing accounting and tax software are able to handle VAT but are not capable of handling corporation tax in real-time or structured reporting at scale, without which the MTD for corporation tax cannot be achieved.

Practice Capacity Concerns

All accounting practices are spread thin due to the implementation of MTD for VAT and the upcoming implementation of Income Tax. HMRC assessed that adding MTD for corporation tax would lead to a complete breakdown of filing and payments with far-reaching effects on the UK economy.

Doubts in Reducing the Corporation Tax Gap

One of the major reasons why HMRC initiated MTD for corporation tax was to reduce the errors and mistakes that were contributing towards the tax gap. Recent studies suggest that MTD might not deliver the results that HMRC was expecting. Hence, to further analyse it, HMRC paused its implementation.

However, it must be understood that making tax digital for corporation tax is paused, not dead.

What the Pause Means for UK Accounting Practices

The pause in the implementation of MTD for corporation tax has given a breathing space for practices to be ready. But some practices are misreading the situation by thinking.

- Corporation tax will remain manual forever

- CT600 processes won’t change

- Digital corporation tax reporting won’t return

What it does mean is:

HMRC has paused the implementation not to shut the MTD for corporation tax down, but to tackle the hindrances and take implementation lessons from VAT and ITSA rollouts.

When MTD for corporation tax eventually returns, it will likely require:

- Cleaner digital records

- Better integration between accounts and tax

- Stronger audit trails

- More standardised workflows

Practices that delay modernisation will feel the heat first.

How UK Accountants Should Prepare for MTD for Corporation Tax

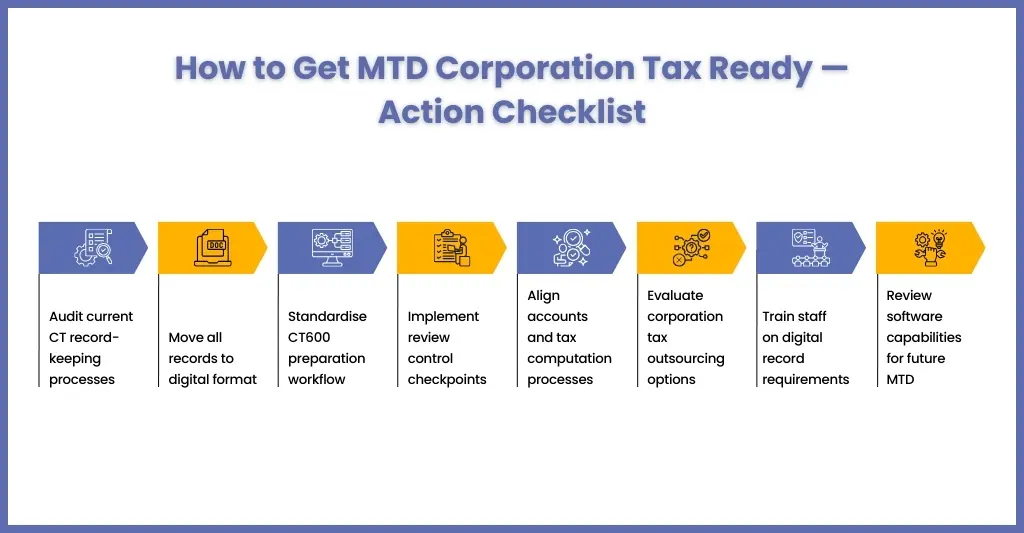

It’s time for UK-based accountants and practices to use the breathing space provided by the pause on the implementation of MTD for Corporation Tax. That space must be utilised to become MTD-ready, and smart practices have already started doing that.

Here’s what you need to do:

Strengthening Digital Record-Keeping

By keeping all the records in digital format, you will ensure bookkeeping feeds are accurate and streamlined into statutory accounts and tax computations.

Standardising CT600 Preparation

Start preparing processes that will standardise CT600 preparation, which include automation or avail corporation tax outsourcing services. This will reduce your reliance on individual judgment and undocumented adjustments.

Improving Review Controls

Having review control checkpoints and improving existing ones will reduce the risk of errors that happen during submissions.

Aligning Accounts and Tax Processes

The tighter the link between accounts and CT computation, the easier future digital reporting becomes.

Whether the MTD for corporation tax will be implemented or not, but by implementing these preparations, you will benefit now, not just later.

MTD for Corporation Tax vs MTD for VAT – Key Differences

| Area | MTD for VAT | MTD for Corporation Tax |

| Nature | Transactional | Judgement-based |

| Frequency | Quarterly | Likely annual or structured |

| Data | Box totals | Accounts + adjustments |

| Complexity | Moderate | High |

| Risk | Filing errors | Technical and compliance risk |

Strategic Opportunities for Forward-Thinking Firms

Some of your counterparts might view MTD for corporation tax as a headache that they will deal with in the future, but others are thinking of it as an opportunity.

Digitally mature practice gains:

- Faster CT600 turnaround

- Reduced rework and corrections

- Better internal capacity management

- Outsourcing the corporation tax work

- More time for advisory services

When the corporation tax compliance is structured beforehand, you will be freeing up your resources for high-value advisory work. That’s where you can generate profits. Currently, we see practices increasingly redesigning their corporation tax processes, not just to be MTD ready, but because efficiency demands it.

Frequently Asked Questions About MTD for Corporation Tax

What is making tax digital for corporation tax?

MTD for Corporation Tax was proposed by HMRC to expand the MTD initiative beyond VAT and Income Tax Self-Assessment. Under MTD for Corporation tax, your clients will need to:

1. Keep digital records for corporation tax

2. Submit corporation tax data digitally

3. Potentially move towards more frequent or structured reporting

Will MTD for corporation tax replace the CT600?

The CT600 will remain relevant for the foreseeable future.

Should UK accountants still prepare for MTD for corporation tax?

Yes. Preparing processes now reduces risk, improves efficiency, and positions your practice ahead of future reform.

Is MTD for corporation tax Cancelled?

HMRC’s July 2025 roadmap states no current plans to introduce MTD for corporation tax.

Conclusion: Digital Corporation Tax Is Delayed — Not Irrelevant

HMRC is very much interested in digitising the entire UK tax process, including corporation tax, hence the pause, not discard. The success or challenges of MTD for Income Tax Self-Assessment, when it launches in 2026, will likely influence how HMRC approaches future digital initiatives across the tax system.

Now, if HMRC decides to implement MTD for corporation tax, you should be ready to handle it. Making your corporation tax processes MTD ready beforehand will give you rich dividends like:

- Clean digital systems

- Structured workflows

- Strong review discipline

Those still reliant on fragmented processes will be sucked into last-minute firefighting, which you must avoid. One way of being MTD corporation tax ready is by availing the corporation tax outsourcing services. Here’s where Corient comes in.

At Corient, we support accounting practices in strengthening their corporation tax preparation, not just for future MTD, but for better control, scalability, and profitability today.

Make your corporation tax service MTD ready by connecting with us. After all, it is better to buy the umbrella before the rain rather than after.