CT600 was supposed to be done by accounting practices without much hindrance, yet many are facing challenges in completing this compliance task effectively, leading to last-minute rushes and late-night checks. It’s a stress that no one is taking into account.

Corporation tax is at its peak of 25% for profits above £250,000, increased scrutiny around R&D claims, and tighter filing enforcement by HMRC have made it even more important to get the CT600 filing right at the first place.

Let’s break it down CT600 properly and make it manageable.

What Is CT600?

A CT600 is the corporation tax return form that limited companies in the UK, foreign companies with UK branches, and clubs/associations must file with HMRC annually.

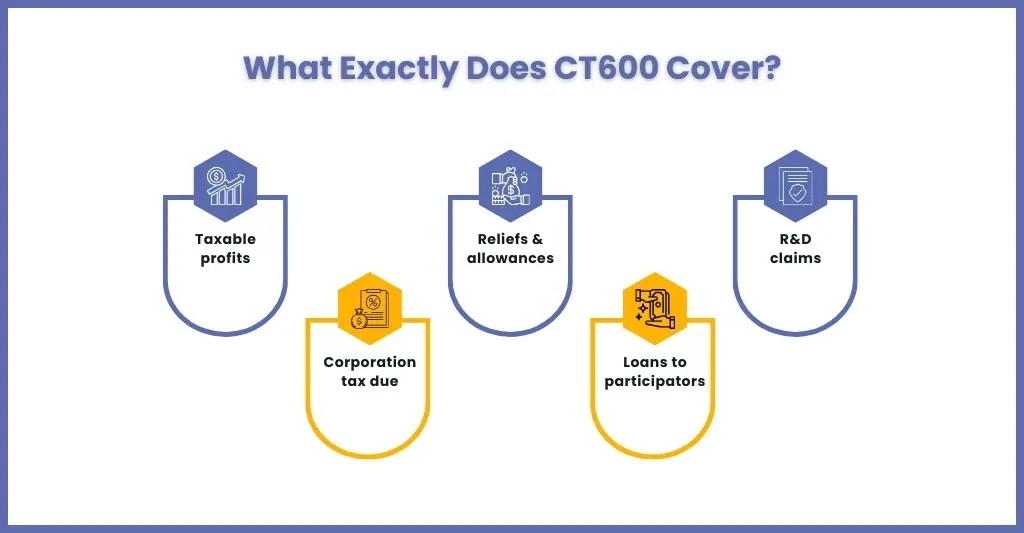

It tells HMRC:

- Company taxable profits

- Corporation tax owed

- Reliefs and allowances claimed

- Loans to participators

- R&D tax credits (where applicable)

This form must be filed electronically using approved software within 12 months of the accounting period. Non-compliance will have legal consequences.

Which of Your Clients Must File a CT600 Form?

All limited companies and organisations in the UK registered with Companies House are required to file a CT600 form. This includes limited companies, foreign companies with UK branches, and clubs or co-operatives. Your clients are still liable to fill the CT600 form even if they make a loss or have no Corporation Tax to pay.

Understanding the CT600 Form — A Section-by-Section Guide for Accountants

A CT600 form is the UK corporation tax return submitted to HMRC, containing your client company’s financial details for an accounting period to calculate tax owed.

Here’s what this form contains:

- Company Details: Under it comes the registered name, UTR (Unique Taxpayer Reference), and the specific accounting period covered.

- Income and Profits: In this section, all your client company’s turnover, trading profits or losses, and other income like bank interest are added.

- Tax Calculation: Total profit, deductions, reliefs (e.g., R&D), and the final Corporation Tax due are included.

- Capital Allowances: Adjustments for equipment purchases and assets.

- Supplementary Pages: Used for specific circumstances such as charitable, exemptions, or foreign income.

CT600 Deadlines and Payment Dates

Deadlines associated with corporation tax have often confused your clients. Here’s something that you will need to remember:

- The CT600 filing deadline is 12 months after the accounting period end

- The corporation tax payment deadline is 9 months and 1 day after the accounting period end

For example, if your clients’ accounting year ends on 31 October 2025, the CT payment is due by 1 August 2026, while the CT600 filing deadline is 31 October 2026. Ideally, it is important for you and your client to complete the filing and payment before August.

Missing the payment deadline will lead to the application of interest, and missing the filing deadline will lead to penalties immediately.

HMRC Penalties Your Clients Will Face for Late CT600 Filings

These days, HMRC has been very strict when it comes to enforcing corporation tax compliance. To maintain and improve compliance, HMRC has been using the penalty tool very effectively.

Penalties for late CT600 filings are:

- £100 immediately if late

- Another £100 if more than 3 months late

- 10% of unpaid tax if 6 months late

- Additional 10% if 12 months late

As an accounting practice handling the corporation tax filings for your clients, it is your responsibility to ensure the deadlines for filing and payment of corporation tax are met. Or else it will negatively impact your clients and your reputation.

Step-by-Step CT600 Filing Process for UK Accountants

Here’s a clean workflow that your practice must follow while filing CT600 for your clients.

Gather All the Records

Gather and prepare all the necessary records from your client, such as company accounts, profit and loss, and details of relief and allowances.

Confirm Accounting Period

Confirm the start and end dates of your clients’ corporation tax period, and also make your client aware of it.

Work Out Taxable Profits

Begin by calculating your client’s profits and then work on the allowances and reliefs.

Complete CT600

Once the calculations are done, begin filling the form by entering your clients’ company details, financial results, tax breaks, and corporation tax calculations.

File Online

Submit the CT600 form through HMRC’s online service or through approved software.

Pay Corporation Tax

Once the submission of the form is done, ensure your client settles the bill within nine months and one day, which is the deadline for corporation tax payment.

Keep Records

Maintain the record of the CT600 and supporting documents after the end of the accounting period, as it will come in handy for audit and future references.

Best CT600 Software for UK Accounting Practices in 2026

HMRC has made it compulsory to use approved software for digital filing. Reason for this is from April 2026, HMRC will shut down its own free online CT600 filing tool. All accounting practices using the online CT600 filing tool must transition to HMRC-approved commercial software. This makes software selection more critical than ever for your practice.

Some of the popular platforms that you must try out are:

- IRIS

- TaxCalc

- BTCSoftware

- CCH

- Digita

Select the software after considering:

- Volume of clients you handle

- Integration with other accounts software

- Requirement of workflow automation needs

Focus must be placed on the software because, through it, you will be able to file CT600 for your clients. But equal attention must also be placed on the process of preparing them. Most accounting practices are unable to get that balance due to multiple factors like volume, complexity and so on. They have turned towards corporation tax outsourcing services for assistance and to get that balance. It’s time for you to make that turn.

Common CT600 Errors That Accountants Must Avoid

There is a possibility that even your experienced accounting team might commit mistakes in CT600 filings. Most of these mistakes happens due to the rise in complexities, short deadlines, and high volumes, leading to pressure. When pressure rises, errors occur.

Let’s break down the most common mistakes you will face and how to prevent them.

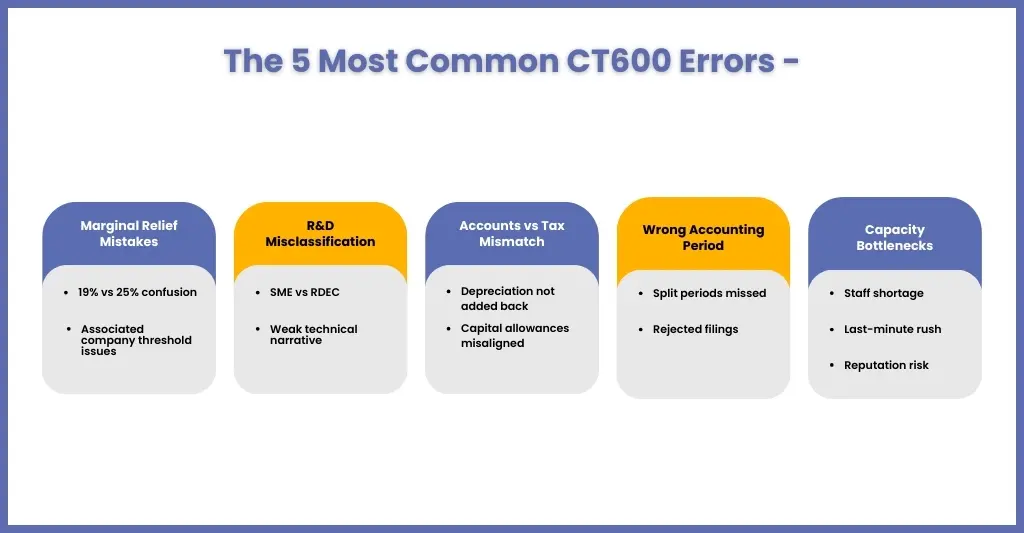

Incorrect Marginal Relief Calculation

Since the reintroduction of the 25% corporation tax main rate, marginal relief calculations have become more complex.

Accountants must consider:

- Small profit rate (19%)

- Main rate (25%)

- Marginal relief band (£50,000–£250,000)

- Associated companies affecting thresholds

A small negligence in oversight, such as failing to adjust thresholds for associated companies, will lead to wrong tax liability.

How to avoid it:

- Always confirm with your client about their associated company status

- Use updated tax software reflecting current corporation tax rates

- Build a review checkpoint for marginal relief cases

R&D Claim Misclassification

R&D claims have become a major compliance hurdle with HMRC increasing its scrutiny due to its misuse and inaccurate submissions in recent years.

Common issues include:

- Claiming routine software upgrades as R&D

- Incorrect SME vs RDEC classification

- Inadequate technical narrative documentation

- Overstated qualifying expenditure

Incorrect R&D reporting on the form can cause enquiries, repayment demands, or penalties.

How to avoid it:

- Validate eligibility criteria carefully

- Ensure technical justifications are documented

- Separate qualifying and non-qualifying costs clearly

- Use specialist review for high-value claims

R&D claims are important for reducing your client’s corporation tax, but they must be defensible.

Mismatch Between Accounts and Tax Computation

It is one of the common and avoidable errors where the profit per statutory accounts does not reconcile with the starting point in the tax computation. HMRC might flag the inconsistencies.

Causes for this mismatch could be:

- Adjustments missed in the tax comp

- Depreciation was not properly added back

- Capital allowances misaligned

- Dividends treated incorrectly

Even small mismatches create:

- HMRC queries

- Processing delays

- Client anxiety

How to avoid it:

- Always reconcile profit before tax to taxable profit

- Run a final cross-check before submission

- Use a structured CT600 preparation checklist

Accuracy in reconciliation reduces risk dramatically.

Filing for the Incorrect Accounting Period

When your client shortens their accounting period, extends their year-end, or changes company structure, the problems start. The CT600 must reflect the correct accounting period, and sometimes more than one return may be required.

Errors here can result in:

- Rejected filings

- Duplicate returns

- Incorrect tax calculations

- Payment mismatches

How to avoid it:

- Confirm Companies House filing period

- Confirm the corporation tax period with HMRC

- Document year-end changes clearly

- Split long accounting periods correctly (if exceeding 12 months)

Late Filing Due to Capacity Issues

Many accounting practices these days are suffering from capacity constraints due to accountant shortages in the UK market. On the other hand, the volume of CT600 filings is rising along with other factors like bottlenecks, last-minute client queries, and staff absences, leading to delays in filings.

Late CT600 filing penalties from HMRC begin at £100 and escalate quickly, and repeated late filings increase penalties significantly.

But here’s the bigger risk:

- Client frustration

- Lost trust

- Damaged reputation

How to avoid it:

- Start CT600 preparation earlier in the cycle

- Spread workloads quarterly

- Standardise preparation processes

- Use structured review workflows

Consider expanding your capacity by availing the corporation tax outsourcing services during peak periods.

It’s time for you to work smarter, not harder!

People Also Ask

What is CT600 and who needs to file it?

A CT600 is the corporation tax return form that limited companies in the UK, foreign companies with UK branches, and clubs/associations must file with HMRC annually.

How does the corporation tax rate affect what I put in the CT600?

You will need to apply the right corporation tax rate (25%, 19%, or marginal relief) based on profit thresholds for the relevant accounting period.

What are the CT600 filing deadlines for UK companies in 2025/26?

The CT600 filing deadline is 12 months after the accounting period end. The corporation tax payment deadline is 9 months and 1 day after the accounting period end.

What is the difference between CT600 and CT603?

The CT603 is simply a notice from HMRC to request the filing of your CT600.

Can a CT600 be longer than 12 months?

As specified in the HMRC guidance, accounting period for Corporation Tax can only be for a period up to 12 months.

Do you have to file a CT600 for a dormant company?

If your clients’ company is dormant, there is no need to fill out a Company Tax Return (Form CT600) for Corporation Tax unless HMRC asks to do it.

Conclusion

Hear us out loud! CT600 does not help your accounting firm to grow; it constrains you. Yes, it is mandatory, but it is repetitive, compliance-heavy, and capacity-draining. As an experienced accounting practice owner, you will need to ask yourself a question: “Should my senior team be preparing CT600 returns or advising clients on growth?”

Enter Corient, an accounting outsourcing service provider serving accounting practices in the UK since 2011. We support accounting practices with structured, compliant, review-ready CT600 preparation through our corporation tax outsourcing services and act as a seamless extension of your team.

Keep your clients satisfied by connecting with us and transforming your CT600 filing process.