UK corporation tax rates no longer involve applying one percentage to a company’s profits. In 2026, UK businesses are facing a corporation tax system where different tax rates are applicable for different profit levels and eligibility for marginal relief. For your accounting practice, this means greater responsibility to ensure calculations are right and your clients pay the right amount of tax.

Let’s understand the importance of getting corporation tax right through an example. One of the practices had a client who was expected to pay 19% corporation tax based on what was paid in the previous years. Until it was discovered that, after examining the clients’ profits and ownership structure, it was eligible for the marginal relief band. The calculations were complex, but the client avoided a surprise tax bill.

This example shows us that corporation tax planning has transformed from a compliance work into an advisory service. Your accountants are required to know about the latest rules that can help your clients save money, improve cash flow, and make better business decisions.

In this practical guide, we’ll break down the current corporation tax rates, explain how they work in practice, highlight common mistakes, and explore how accountants can turn tax complexity into an opportunity to deliver greater value.

What is the Corporation Tax Rate in the UK?

The UK corporation tax rate is 19% for profits under £50,000 (small profits rate), 25% for profits over £250,000 (main rate), and between 19–25% via marginal relief for profits between £50,000 and £250,000. These thresholds are divided between associated companies.

The taxable profits for corporation tax that your clients make will include:

- Trading profits

- Investment income

- Chargeable gains from asset sales

The corporation tax rate depends on the company’s profit levels and whether it has associated companies.

The current corporation tax rates are:

- 19% Small Profits Rate

- 25% Main Rate

- A rate between 19% and 25% through Marginal Relief

How Corporation Tax Rates Work in Practice

The corporation tax structure was introduced in April 2023, and it still remains in place in 2026.

Here are the current and previous corporation tax rates:

| Rate | 2026 | 2025 | 2024 | 2023 | 2022 |

| Small profits rate (companies with profits under £50,000) | 19% | 19 % | 19% | 19% | — |

| Main rate (companies with profits over £250,000) | 25% | 25% | 25% | 25% | — |

| Main rate (all profits except ring fence profits) | — | — | — | — | 19% |

| Marginal Relief lower limit | £50,000 | £50,000 | £50,000 | £50,000 | — |

| Marginal Relief upper limit | £250,000 | £250,000 | £250,000 | £250,000 | — |

Now, how does it work? Let’s look at three businesses.

Company Taxable Profit Tax Position

| Company | Taxable Profit | Tax Position |

| Company A | £40,000 | Small Profits Rate (19%) |

| Company B | £120,000 | Marginal Relief Applies |

| Company C | £350,000 | Main Rate (25%) |

The marginal relief formula is Marginal Relief = (U−A)×UN×F

Where:

- U = Upper profit limit (£250,000)

- A = Augmented profits (taxable profits plus exempt distributions)

- N = Taxable total profits

- F = Marginal relief fraction (3/200)

(250,000−100,000)×250,000100,000×2003

Marginal Relief = £900

According to HMRC, Corporation Tax remains one of the largest sources of business taxation revenue in the UK, generating £97.2 billion in total receipts from all corporate taxes for 2024 to 2025. Accurate compliance and planning, therefore, remain a major focus for both your clients and tax authorities.

Associated Companies and Their Impact on Corporation Tax Rates

One of the most misunderstood areas of corporation tax involves associated companies.

What Are Associated Companies?

Companies are generally associated when one company controls another or when multiple companies are under common control.

Why Does This Matter?

Because the corporation tax thresholds are divided between associated companies.

The £50,000 and £250,000 thresholds do not automatically apply to each company individually.

Example

Suppose an individual owns:

- Company A

- Company B

The thresholds may be split between the two companies.

Instead of:

- £50,000 lower threshold

- £250,000 upper threshold

Each company may effectively receive:

- £25,000 lower threshold

- £125,000 upper threshold

As a result, businesses may enter marginal relief or main-rate taxation much sooner than expected.

This is an area where accountants frequently add significant value through planning and forecasting.

Corporation Tax Payment Methods in the UK

Once a company has calculated its Corporation Tax liability, it must pay HMRC by the relevant deadline. For most small and medium-sized companies, Corporation Tax is due 9 months and 1 day after the end of the accounting period.

Online or Telephone Banking (Faster Payments, CHAPS, or Bacs)

This is the most commonly used payment method.

Clients can make Corporation Tax payments can be made directly from their bank account using:

- Faster Payments

- CHAPS

- Bacs

When making the payment, they must use their 17-character Corporation Tax payment reference number so HMRC can allocate the payment correctly.

Debit Card or Corporate Credit Card

They can pay Corporation Tax online through HMRC’s payment portal using:

- Debit cards

- Corporate credit cards

Personal credit cards are generally not accepted for Corporation Tax payments.

Direct Debit

Set up a Direct Debit through their HMRC online account. This option can be useful for clients that prefer automated payments and want to reduce the risk of missing deadlines.

Through a bank or Building Society

Some banks allow Corporation Tax payments to be made in person at a branch, although this option has become less common as HMRC encourages digital payments.

Through an Accountant or Agent

Your accountants can manage tax payments and reminders. While accountants cannot usually make payments directly from a client’s bank account, they can help ensure deadlines are met and payment references are used correctly.

Why Corporation Tax Rates Are More Complex for Accountants in 2026

Corporation tax looks simple, but it’s not due to several reasons. These reasons are:

Multiple Tax Bands

Since 2023, multiple tax rates have been introduced, which means calculations are no longer straightforward.

Associated Company Rules

There have been multiple instances where one company controls another one or multiple companies. In such a situation, ownership structures must be reviewed carefully.

Increased HMRC Scrutiny

HMRC is interested in expanding its Making Tax Digital initiative from VAT and Income Tax to corporation tax. According to HMRC, digital tax administration and compliance have helped the government in improving tax collection.

Greater Client Expectations

Clients are increasingly expecting practices to provide:

- Tax planning advice

- Cash flow forecasting

- Profit extraction strategies

- Business growth guidance

As a result, corporation tax has become both a compliance challenge and an advisory opportunity.

Common Mistakes Accountants Make with Corporation Tax Rates

Even with years of experience, experienced accounting practices commit some mistakes when it comes to corporation tax rates. Some of those common mistakes are:

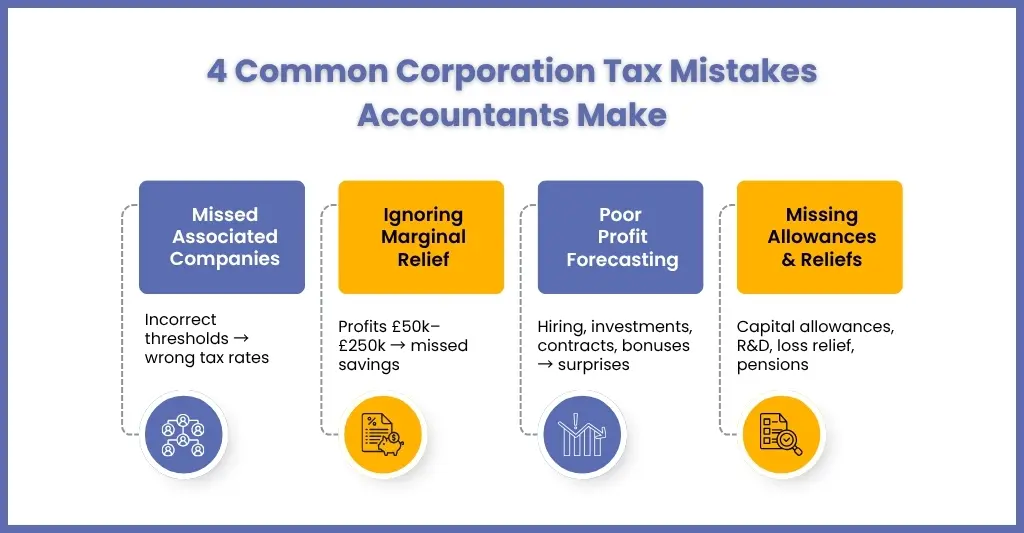

Failing to Identify Associated Companies

It remains one of the most persistent errors committed by practices across. Since the introduction of the current corporation tax regime, the profit thresholds for the Small Profits Rate and Main Rate are divided among associated companies. Missing out on associated company relations will lead to inaccuracies in tax calculations.

Ignoring Marginal Relief

There have been instances where practices solely focus on headline rates (25% and 19%) and ignore marginal relief opportunities. Many companies with profits between £50,000 and £250,000 generally fall into the marginal relief band, meaning their effective tax rate sits somewhere between the two. This will lead to inaccuracy in forecasts and missed tax planning opportunities.

Poor Profit Forecasting

The client depends on your forecasting so that decisions can be made that will affect their taxable profits.

Businesses constantly make decisions that affect taxable profits, including:

- Hiring new employees

- Purchasing equipment

- Investing in technology

- Taking on additional contracts

- Expanding into new markets

- Paying director bonuses

Without regular and accurate forecasting, tax surprises will become more common.

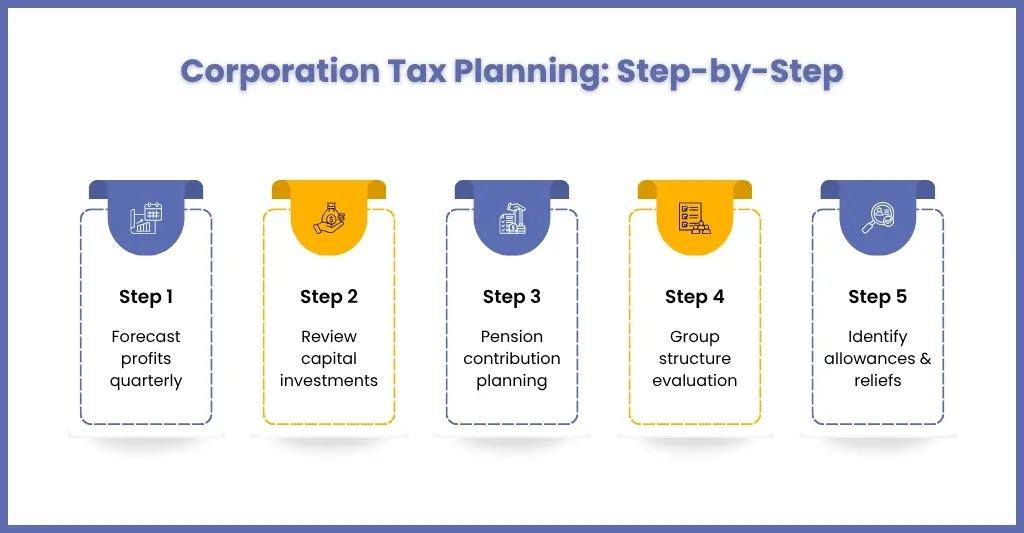

Missing Allowances and Reliefs

Many of your clients fail to maximise:

- Capital allowances

- Research and Development reliefs

- Loss relief opportunities

- Pension contribution planning

A proactive approach often produces better outcomes.

How Accountants Can Optimise Corporation Tax for Clients

While your clients can escape from the corporation tax rates, you can help them reduce their tax by carefully managing their tax liabilities.

Here’s how it is done.

Regular Profit Forecasting

One of the most powerful tax-planning tools available to accountants is regular profit forecasting. Many business owners only think about corporation tax when their year-end accounts are being prepared. By then, opportunities to reduce tax liabilities may already have been missed.

Through forecasting, you can identify the potential tax exposures well before year-end, which gives time for your clients to act upon.

Review Capital Investment Plans

Many companies purchase equipment, machinery, vehicles, software, and office technology throughout the year. However, without proper planning, clients may fail to maximise the tax relief available on these purchases.

Conduct frequent reviews of your client’s capital investment plans so that they time their asset purchases correctly. This way, they can maximise their allowances.

Consider Pension Contributions

Pension contributions still remain one of the most effective ways to reduce corporation tax liabilities. Employer contributions are generally treated as a deductible business expense, meaning they can reduce taxable profits while simultaneously helping directors and employees build retirement savings.

For clients, this can provide multiple advantages:

- Lower corporation tax liability

- Improved retirement planning

- Efficient profit extraction

- Potential National Insurance savings

Evaluate Group Structures

The corporation tax landscape became more complex with the introduction of the current tiered tax system. As a result, ownership structures now play a more important role in determining tax liabilities.

Associated companies can significantly affect corporation tax thresholds because the lower and upper profit limits are divided between qualifying companies.

Regular reviews can help:

- Identify potential tax risks

- Ensure compliance with associated company rules

- Support business restructuring decisions

- Improve future tax planning

Focus on Advisory Services

The role of accountants is changing. Historically, many firms generated the majority of their revenue through compliance services such as bookkeeping, payroll, VAT returns, and year-end accounts.

Today, clients increasingly expect strategic advice.

Many practices are therefore looking for ways to free up internal capacity, so their senior staff can focus on tax planning and client advisory work.

This is where corporation tax outsourcing services can play an important role.

By partnering with providers like Corient, accounting firms can delegate routine accounting, bookkeeping, payroll, and compliance tasks while retaining control of client relationships and high-value advisory services.

Key Deadlines Linked to Corporation Tax (For Accountants)

Missing deadlines can result in penalties and unnecessary stress for clients.

Corporation Tax Payment

The payment of corporation tax is generally due at 9 months and 1 day after the end of the accounting period

Company Tax Return (CT600)

CT600 is generally due 12 months after the end of the accounting period

FAQs on Corporation Tax Rates for Accountants

What are the current corporation tax rates in the UK for 2026?

The current rates are:

a. 19% Small Profits Rate for profits up to £50,000

b. 25% Main Rate for profits above £250,000

c. Marginal Relief applies between £50,000 and £250,000

Associated companies may reduce these thresholds.

Do associated companies affect corporation tax rates?

Yes. Associated companies generally share the lower and upper profit thresholds, which can move companies into higher tax bands sooner than expected.

How can accountants reduce corporate tax liability for clients?

Accountants can help clients optimise corporation tax through forecasting, capital allowance planning, pension contributions, relief claims, profit extraction strategies, and careful business structuring.

What brings down Corporation Tax?

There are a number of legal ways that business owners can reduce their Corporation Tax bill. These include making additional pension contributions, making charitable contributions, and investing in research and development.

Who is exempt from Corporation Tax?

Charities are, in general, exempt from giving corporation tax, nevertheless they have to compute and submit corporation tax returns if they have: Any taxable gains or income which are not covered by an exemption or relief.

Conclusion: Turning Corporation Tax Complexity into an Advisory Opportunity

Corporation tax rates have become much more complex for your clients to realise. Between multiple tax bands, marginal relief calculations, associated company rules, and increasing compliance expectations, there is plenty of room for confusion.

But this complexity creates an opportunity for you.

If you have a grip on the corporation tax rates and regulations, you will be in a position to provide valuable guidance, help your clients avoid making mistakes, and identify tax-saving opportunities. More importantly, you can position yourself as trusted advisors rather than compliance providers.

In case the advisory work grows more than your capacity, then partner with trusted outsourcing partners like Corient, which will free up time for higher-value corporation tax planning and strategic client support.

Contact us and deliver insight, build stronger relationships, and create long-term growth opportunities for your clients.