UK GAAP changes in 2026: Are you really ready for them? We have an honest answer for you: no, you are not. While it’s good that you are aware of the changes to UK GAAP, that’s not enough; you need to invest in updating your workflows, systems, and bookkeeping processes to handle them effectively.

Let’s understand this through a real situation.

A UK-based accounting practice has already done accurate year-end accounts under Financial Reporting Standards 102 (FRS 102). But during the recent audit, the practice came face to face with unexpected queries around revenue recognition and lease accounting, areas impacted by the new UK GAAP changes.

This issue was created because the day-to-day bookkeeping workflows had not been updated as per the new requirements.

The result of it was:

- Delayed audit completion

- Additional rework

- Increased client pressure

The goal of the updates by the Financial Reporting Council (FRC) of FRS 102 is to bring the UK GAAP in line with International Financial Reporting Standards (IFRS). But it has also introduced a new complexity for accounting practices and their clients.

It’s not enough to understand the rules; you need to ensure your entire workflow is audit-ready.

What Are the Latest Changes to UK GAAP?

FRS 102 is a single financial reporting standard that applies to the financial statements of UK entities that are not applying IFRS as adopted by the UK. The latest changes to the UK GAAP, especially to the FRS 102, have been implemented from 1 January 2026 for more transparency and to align it with IFRS.

It is important to note that these changes are going to have a significant impact on financial statements, which are:

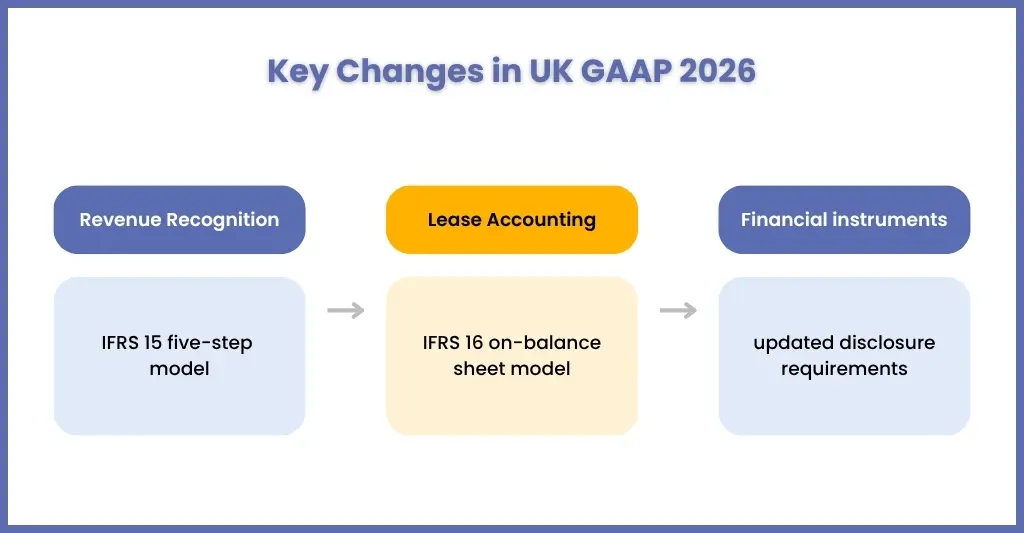

- The revised revenue accounting requirements in FRS 102 and FRS 105 for revenue recognition are based on the IFRS 15 five-step model.

- Updated lease accounting requirements in FRS 102 as per the IFRS 16′ on-balance sheet’ model for simplification, bringing in more leases brought onto the balance sheet.

These changes are not going to impact year-end accounts, but the way transactions will be recorded throughout the year.

What These UK GAAP Changes Mean for Your Financial Reporting

When it came to these changes in UK GAAP, we have come across many accounting practices telling us, “We’ll deal with this at year-end”. But that’s a risky thing to do.

Why?

Because these changes will affect:

- In what way is revenue recorded

- How leases are treated

- How financial data is structured

They do not even inform their clients about the changes in FRS 102 with the 2025 IRIS report showing that 24% of businesses were unaware of the changes, with many at risk of non-compliance.

If your bookkeeping services and your clients are not aligned with the latest changes, then you will face:

- Multiple reworks in the financial statements you prepared

- Longer audits

- Increase in compliance risk

Practices that incorporate the changes in UK GAAP the earliest will be less likely to stress during audits, causing a rise in costs and delays.

Common Pitfalls for Accounting Teams Under the New UK GAAP

Understanding the new UK GAAP changes is more than just reading them. We have often encountered accounting teams struggling with it, not due to a lack of technical knowledge, but because their workflows, processes, and systems have not evolved as per present compliance requirements. Let’s understand these pitfalls.

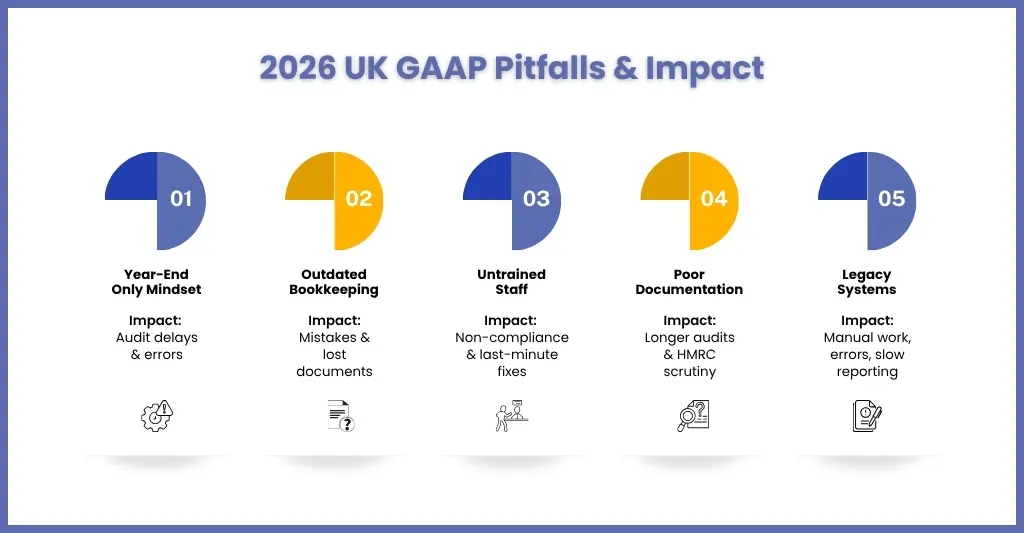

Treating Changes as Year-End Only

One of the biggest mistakes firms make is assuming that UK GAAP changes are relevant only at the year-end audit.

This is one of the biggest mistakes that many practitioners make when it comes to UK GAAP changes. In reality, these new rules around revenue recognition, lease accounting, and financial instruments impact the daily bookkeeping entries and transactions.

Impact:

In case these adjustments are not incorporated right at the beginning, then your accountants will have to face multiple corrections at the year-end, leading to:

- Delay audit completion

- Surge the risk of errors

- HMRC queries

Compliance with new UK GAAP is a continuous responsibility. You must integrate these updated standards into daily workflows to avoid last-minute chaos.

Outdated Bookkeeping Processes

Are you still relying on manual processes, spreadsheets, or inconsistent categorisation? There was a time these used to work, but not anymore, especially under the new reporting standards.

- Hand-typed entries and paper records increase the possibility of errors.

- Different accountants may classify similar transactions differently, leading to audit discrepancies.

- Loss of receipts, incomplete documentation, or unverified journal entries will compromise audit integrity.

Impact:

Such outdated bookkeeping processes will create red flags for auditors. Even small errors in classification will lead to significant challenges, especially with new disclosure requirements.

The best way to avoid this mistake is to transform your bookkeeping by adopting cloud-based accounting solutions or avail bookkeeping outsourcing from professional providers like Corient.

Lack of Staff Training

Depending on software updates is not enough; you will need to train your accounting staff to reduce their knowledge gap when it comes to these new standards.

- New Revenue Recognition Rules: Your staff must know how to allocate revenue over multiple performance obligations rather than at a single point.

- Lease Accounting Changes: Accountants must correctly identify on- and off-balance sheet leases, calculate right-of-use assets, and adjust depreciation.

- Disclosure Requirements: Your teams must know how to prepare financial notes that satisfy auditors.

Impact:

Without proper training, even the best bookkeeping practices can result in:

- Errors in financial statements

- Non-compliance with FRS 102

- Hurried last-minute corrections that increase your workload and penalty risks

To negate this, you will need to conduct quarterly internal training schedules for your staff, or an even better way is to use the services of a professional outsourcing provider like Corient. They will effectively guide your staff in the application of new standards correctly in day-to-day workflows.

Poor Documentation

Apart from accurate numbers, an auditor will also demand evidence to back them, and that’s only possible through proper documentation of transactions.

These documents contain:

- Audit Trails: Each transaction or adjustment must be traced from the source document to the final report.

- Detailed Explanations: Narrative notes should explain assumptions, valuation methods, and accounting judgments.

- Consistent Records: Discrepancies across spreadsheets, ledgers, or software modules can delay audits and trigger queries.

The impact of poor documentation will lead to:

- More audit time and fees

- Delayed client reporting

- Reputational risk for your practice if HMRC flags incomplete or inconsistent submissions

To avoid this, you must invest in a centralised document management system that stores all the source files, approvals, and commentary linked directly to financial transactions. Providers like Corient can help you in integrating documentation workflows into daily accounting tasks to ensure audit readiness.

Over-Reliance on Legacy Systems

We have noticed multiple practices still relying on outdated accounting software that are not designed for handling 2026 UK GAAP updates.

Older software may not support:

- New revenue recognition formats

- Lease accounting calculations

- Expanded disclosure templates

This will lead to manual workarounds, leading to inconsistencies and duplicate efforts across teams.

The impact of this will be:

- Slow down reporting

- Increase in errors due to manual adjustments

- Making compliance with FRS 102 and MTD integration cumbersome

The solution is to invest in cloud-based, GAAP-compliant accounting software that integrates:

- Real-time reporting

- Automated checks for FRS 102 adjustments

- Multi-user access for accountants, auditors, and clients

Step‑by‑Step Guide to Prepare for 2026 UK GAAP Changes

Knowing the 2026 UK GAAP changes is not enough; you need to integrate them into every step of your accounting workflow. This is where many accounting practices falter by waiting till the year-end to adjust, and by the time they realise it’s too late.

To avoid such a situation for your practice, we have developed a step-by-step guide to stay compliant, reduce errors, and be audit-ready.

Step 1: Assess Current Workflows

Understand where your current processes stand right now by doing the following.

- Review Bookkeeping Processes

Conduct a detailed review of your bookkeeping processes by examining how transactions are currently recorded and identifying gaps that could create errors under the new standards.

- Recognise Gaps in Data Capture

Under the new UK GAAP changes, updated revenue recognition and lease accounting rules require more detailed information, thus ensuring all the important information is captured.

- Check Compliance with New Standards

Compare your current workflow against FRS 102 updates to identify areas of non-compliance.

Create a workflow map for each client type to identify compliance gaps. Using the audit outsourcing services of service providers, you can identify gaps quickly and take remedial measures.

Step 2: Update Accounting Policies

Perform updates in your accounting policies so they fulfil the new UK GAAP requirements. To do that, you will need to:

- Revise Revenue Recognition Policies

The new revenue accounting requirements are aligned with IFRS 15, it means revenue must be recognised over performance obligations rather than at a single point. Updates in your internal guidelines must be carried out accordingly.

- Update Lease Accounting Methods

As per the new rules, certain leases now come onto the balance sheet. This will change how right-of-use assets and lease liabilities are recorded.

- Align with FRS 102 Changes

Ensure that financial statement templates, journal entries, and disclosures meet the updated standard.

Make sure your accounting staff is aware of these policies, and for a smooth integration, you will take the help of outsourcing service providers that offer standardised policy templates.

Step 3: Train Your Team

Even after creating the best process, it will fail if your accountants are not trained or aware of it. So, invest in:

- Teaching Your Staff About UK GAAP Updates

The updates, like revenue recognition and lease accounting, are new for your accountants, and they must be thought about because they affect daily bookkeeping and reporting.

- Explain the Operational Impact

Make your accountants understand the impact of these changes in day-to-day entries, client reporting, and audit readiness.

- Emphasise Documentation Requirements

Focus on maintaining clear and consistent records for auditors and regulators.

Conduct short training sessions for your accountants. Also, practices that use Corient’s services often combine software automation with expert guidance, reducing training overhead while ensuring staff are fully compliant.

Step 4: Upgrade Technology

Old accounting software, legacy systems and manual spreadsheets are not designed to handle the complexity of the new rules. Therefore, you will need to invest in:

- Automated Categorisation

Systems that automatically categorise transactions reduce errors in revenue recognition and lease accounting.

- Real-time Reporting

Cloud-based solutions allow you to track changes throughout the year, ensuring your books are always audit-ready. Through cloud-based solutions, you can track changes all year and ensure your client is audit-ready.

- Audit Trails

All transactions, adjustments, and journal entries must be traceable for compliance and verification.

This ensures automation isn’t just a convenience; it ensures compliance is embedded into your process.

Step 6: Perform Regular Reviews

Don’t wait until the year-end to check compliance; conduct frequent checks. This can be done through

- Quarterly Reviews

Conduct an audit of a sample of transactions every quarter to see its compliance with updated FRS 102 standards.

- Error Tracking

Find discrepancies in the early stage to avoid year-end corrections.

- Client-Specific Adjustments

Some of your clients may have unique transactions that require greater attention, such as multi-property portfolios or foreign assets.

Incorporate automated compliance checks along with manual reviews.

Real World Impacts: Case Studies & Examples

Example 1: Revenue Recognition

A firm incorrectly recognised revenue upfront instead of over time.

Result:

- Audit adjustments required

- Financial statements restated

Example 2: Lease Accounting

Leases are not recorded on the balance sheet under the new rules.

Result:

- Non-compliance

- Audit delays

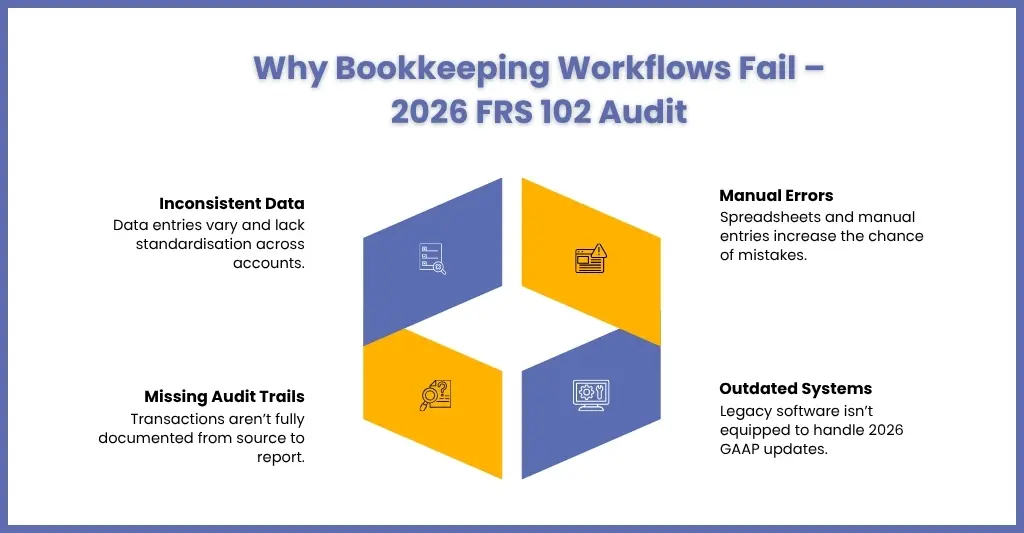

Why Your Bookkeeping Workflow Can Fail a 2026 FRS 102 Audit

There are multiple reasons that can contribute to your bookkeeping workflow failure during a 2026 FRS 102 audit. Let’s become aware of those reasons so that effective action can be taken to negate them.

Inconsistent Data

With the implementation of the 2026 UK GAAP changes, you cannot ignore the lack of proper data management. 2026 UK GAAP updates require accurate data all the time, to avoid different categorisation methods or a lack of standardisation.

Follow a standardised template for categorisation of data.

Missing Audit Trails

Lack of documentation of transactions right from their source will lead to the loss of audit trails. This will cause problems during audits because auditors would like all your transactions, adjustments, and journal entries to be traceable and meet compliance.

Manual Errors

Avoid using manual spreadsheets to avoid errors like incorrect entries and missed adjustments. Even old accounting software and legacy systems are not designed to handle the complexity of the new rules, leading to manual intervention. Hence, focus on getting new accounting software and systems or explore the outsourcing option.

Most of these issues don’t show up until audit, and fixing them is costly and time-consuming, and this is where practices suffer the most. Therefore, to balance the workload and compliance, it is wise to choose outsourcing services to get the job done.

Frequently Asked Questions (FAQ)

What are the key UK GAAP changes practices need to know in 2026?

The key changes under UK GAAP 2026 are the updates to revenue recognition, lease accounting, financial instruments, and disclosure requirements under FRS 102. These changes have impacted the bookkeeping and financial reporting process.

Is early adoption of the new UK GAAP changes permitted?

It’s allowed in certain cases, but practices must ensure full compliance and consistency across financial statements.

How should firms update bookkeeping workflows to prepare for an audit?

Accounting practices should:

a. Standardise processes

b. Automate data capture

c. Maintain clear documentation

d. Conduct regular compliance reviews

Is FRS 102 mandatory?

The Financial Reporting Council’s (FRC’s) second periodic review of FRS 102 will become mandatory for reporting periods beginning on or after 1 January 2026.

Conclusion

The UK GAAP changes in 2026 are not normal technical changes, but they require changes in your bookkeeping process, which increases your workload and compliance requirements.

For accounting practices, this means:

- Updating workflows

- Improving documentation

- Adopting better systems

Without preparation:

- Audits become difficult

- Errors increase

- Compliance risks grow

With the right approach and support from Corient, you can:

- Ensure audit-ready workflows

- Reduce manual effort

- Stay compliant with FRS 102

- Scale your practice confidently

Have you still not updated your bookkeeping process as per 2026 UK GAAP? Not to worry, get connected with us through our contact form, and we will ensure your compliance burden is taken care of.