Here’s a simple way to understand P11D vs P11D(b).

- P11D reports employee benefits and expenses

- P11D(b) reports the total Class 1A National Insurance due on those benefits

But here is where things get confusing for both accounting practices and employers. Let’s explain this situation through a scenario.

An expanding consultancy firm in the UK has been providing company cars, medical insurance and travel reimbursements to its employees. At the year-end, their accounting team submitted P11D forms but completely forgot about P11D(b).

A few weeks later, HMRC issued a penalty notice. The issue wasn’t negligence. There was confusion around P11D vs P11D(b), something that even experienced teams get wrong under pressure. Scarily, these days, even accounting practices are facing the same issue while handling the payroll of their clients.

If you’re managing payroll for multiple clients, then it’s important to negate this compliance risk once and for all.

In this guide, we’ll break down:

- What P11D and P11D(b) actually mean

- Key differences

- 2026 deadlines you cannot miss

- Penalties to avoid

- And how outsourcing can manage this efficiently

What Is a P11D Form

P11D forms are used in reporting benefits in kind and expenses provided by your clients to their employees.

The benefits include:

- Company cars and fuel

- Private medical insurance

- Interest-free or low-interest loans

- Living accommodation

- Certain reimbursed expenses

If a benefit is not included in the payroll, then it must be reported on a P11D. These P11D forms are required by your client employers to submit for each employee who gets tax benefits.

What Is a P11D (b) Form and How Is It Different from P11D

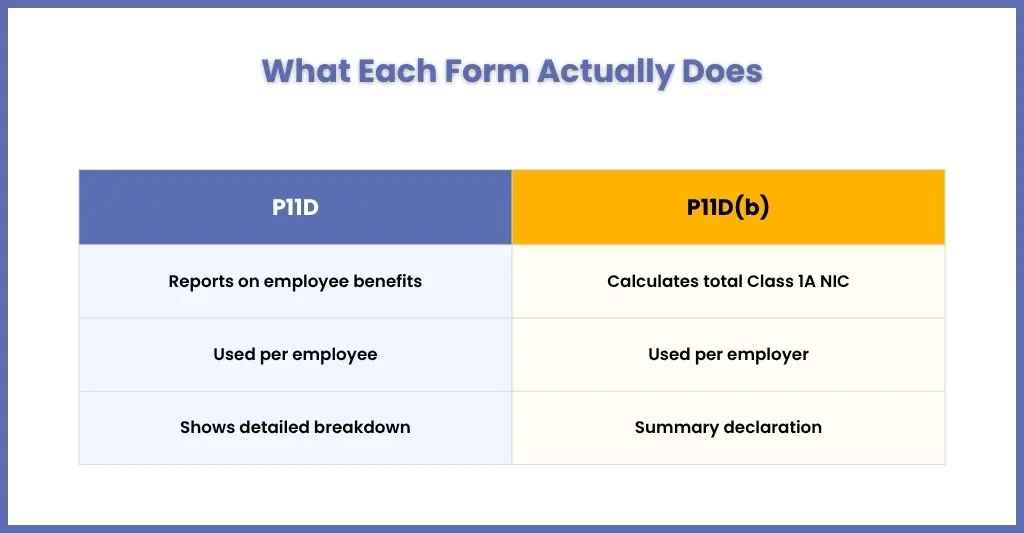

Many practices, employers and employees get confused between P11D and P11D (b). One thing you need to understand is that P11D(b) is the form that your client’s employer must fill out, and it calculates the total Class 1A National Insurance due on all employee benefits. In short, it summarises the information from all P11D forms submitted by their employees.

Unlike P11D, P11D (b) has to be submitted only by the employer, meaning one P11D (b) per employer. It acts as a declaration that all P11Ds are complete and accurate.

P11D vs P11D(b) — Side-by-Side Comparison

| Aspect | P11D | P11D(b) |

| Purpose | Reports individual employee benefits | Calculates employers NI contributions |

| Frequency | One per employee | One per employer |

| Content | Detailed benefit breakdown provided to an employee | Summary calculations |

| Recipients | HMRC and the employee | HMRC only |

| Deadline | 6 July 2026 | 6 July 2026 |

It is wrong to assume P11D vs P11D(b). The first one focuses on employee expenses and benefits, and the second one deals with your client’s employers’ National Insurance obligations. Both works together in the compliance process.

2026 Deadlines You Cannot Afford to Miss

Another point at which many practices get confused is the deadlines associated with P11D and P11D(b).

Let’s end this confusion at once:

- Both forms have to be submitted by 6 July and have to be sent electronically through approved software. Paper submissions are no longer accepted by HMRC.

With regards to payment of Class 1A National Insurance, it has different deadlines:

- Electronic payments: 22 July

- Postal payments: 19 July

Missing out on any of the above-mentioned payment deadlines will attract serious penalties and interest from HMRC.

P11D Penalties – What Happens If You File Late or Incorrectly?

HMRC applies penalties for late submissions of P11D. As per Section 98(1)(b) Taxes Management Act 1970:

- Maximum initial penalty of £300 per form for failure to submit forms P11D

- Continuing penalties of a maximum of £60 per day thereafter, until the failure has been remedied.

Similarly, penalties for the late submission of P11D(b) are:

- £100 per 50 employees for each month

Penalties will also apply if:

- Benefits are underreported

- Forms contain errors

- Class 1A NIC is miscalculated

While managing multiple clients, even small errors across several submissions can quickly become costly and time-consuming. Due to this, many practices have sought assistance through payroll outsourcing services to reduce submission errors and speed up the entire process.

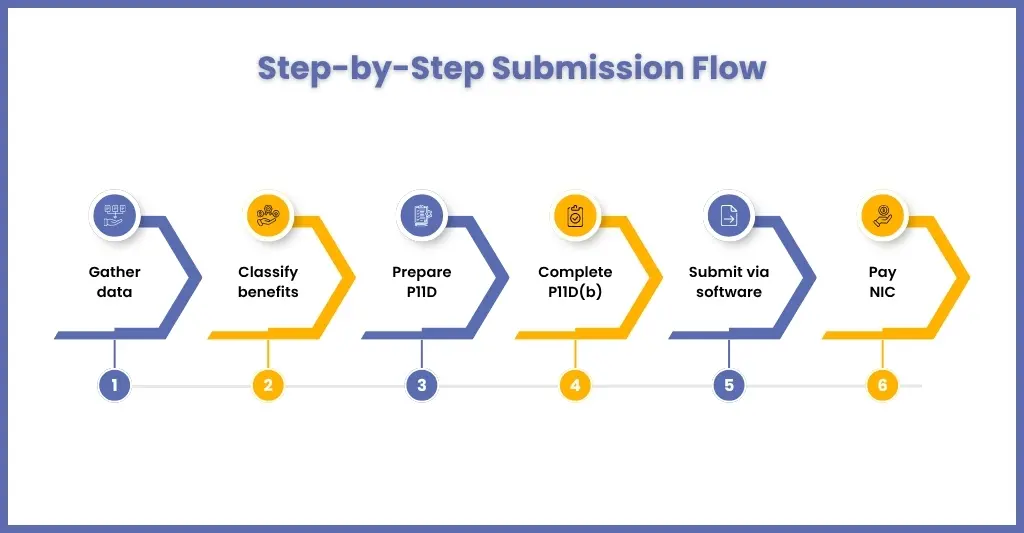

How to Submit P11D and P11D(b) to HMRC — Step by Step

Submitting P11D and P11D(b) requires precision, and most errors happen not because you are unaware of the rules but due to rushed data and last-minute submissions.

Let’s break this down in a way that helps you get it right the first time.

Step 1: Gather Benefits Data

Here’s where it begins, including the mistakes. You will have to collect all the data accurately for the entire tax year (6 April to 5 April).

What data do you need to gather?

- Employee benefits in kind (BIKs)

- Reimbursed expenses

- Payroll records (to identify payroll benefits)

- Company car details (CO₂ emissions, fuel type, availability)

- Private medical insurance values

- Loans or advances provided to employees

- Expense claims and supporting receipts

Step 2: Classify Benefits Correctly

After collecting the data, it must be classified properly, which can be challenging and chances of error occuring.

Classify the benefits as follows:

- Taxable benefits: Must be reported

- Exempt benefits: No reporting required

- Payroll benefits: Already taxed via payroll

Examples:

- Company car: Taxable (report in P11D if not payrolled)

- Private medical insurance: Taxable

- Business travel reimbursements: Often exempt

- Trivial benefits: Usually exempt

For successful classification, maintain a benefit classification guide and cross-check payroll vs non-payroll items. Also, keep an eye on the HMRC guidance annually for any updates. Incorrect classification is one of the biggest reasons for HMRC penalties.

Step 3: Preparing P11D Forms

Start preparing P11D forms for each employee.

Each form must include:

- Employee details (name, NI number, payroll ID)

- Breakdown of benefits received

- Cash equivalent value of each benefit

Get a payroll software to automate the entire process and conduct a thorough review of the forms before submission.

Step 4: Complete P11D(b)

P11D(b) is not just a form; it’s a declaration.

It confirms that:

- All P11Ds are complete and accurate

- Declare total benefits provided

- Calculate total Class 1A NIC liability

It was never P11D vs P11D(b), P11D is the detail, P11D(b) is the financial impact.

Step 5: Submit via HMRC Compatible Software

Once the P11Ds and P11D(b)s are prepared, it’s time to submit them, and it must be done using payroll/accounting software.

The benefit of using the best payroll software is:

- It automates calculations and reduces errors

- Ideal for practices that handle multiple clients

Submit the forms before 6 July, and don’t wait until the deadline passes; chances are, the HMRC system will get overloaded.

Step 6: Pay Class 1A NIC

With submission done, now it’s time for payment.

Make note of these key deadlines:

- 19 July for postal payments

- 22 July for electronic payments

Missing out on these deadlines leads to interest and penalties.

How Corient Helps UK Accounting Practices Manage P11D and P11D(b) Submissions

When it was one client, it was fine, but when you started handling P11D and P11D(b) submissions for multiple clients, things started getting out of hand. During the peak season, you must have faced:

- Workload spikes

- Tight deadlines

- Compliance pressure

- Risk of errors

This is where payroll outsourcing comes as a blessing in disguise, and here’s where Corient comes into the picture.

We support UK accounting practices by managing end-to-end P11D and P11D(b) processes.

Through our payroll outsourcing services, we handle:

- Data collection and validation

- Benefit classification

- Accurate form preparation

- Timely submission

- NIC calculation and reporting

Through our services, you will avoid:

- Compliance risk

- Last-minute rush

- And provide more time towards:

- High-value advisory work

- Scalable services during peak seasons

Frequently Asked Questions About P11D vs P11D(b)

Do I need to submit both P11D and P11D(b)?

Yes. If your client is providing benefits in kind, they are required to submit:

a. P11D (for employees)

b. P11D(b) (for employer NIC declaration)

What is the P11D(b) penalty for late submission?

Penalties for the late submission of P11D(b) are £100 per 50 employees for each month.

What is the difference between P11D and P11D(b) for payrolled benefits?

Under P11D, payrolled benefits are not included. However, in P11(b) still requires to report Class 1A NIC.

What are the P11D deadlines?

6 July 2026 is the deadline to submit your P11Ds and P11D(b) for the 2025/26 tax year.

Is P11D being phased out?

The UK government is planning to replace it with payrolling of benefits in kind (BiKs). It means the benefits must be reported and taxed through payroll in real-time. The original phasing-out date was April 2026, but it has been postponed to April 2027.

Conclusion

It’s important to have a deep understanding of P11D vs P11D(b). Yes, both are different from each other, but both need the same ingredients.

- Accurate data

- Correct classification

- Strict deadlines

- Compliance with HMRC regulations

With increasing reporting complexity, growing client demands, and high volumes, many practices are moving toward outsourced support for efficiency, speed, and scalability. Corient is appearing to tick all the boxes.

By partnering with experts like Corient, you can reduce your:

- Compliance risk

- Improve accuracy

- Handle peak workloads efficiently

- Focus on higher-value services

Avoid firefighting this P11D season by filling out our contact form and staying ahead of deadlines.